WIDE BAND GAP ( WBG) TECHNOLOGIES

A status report for SiC and GaN (by Hong Lin and Ana Villamor of Yole Développement)

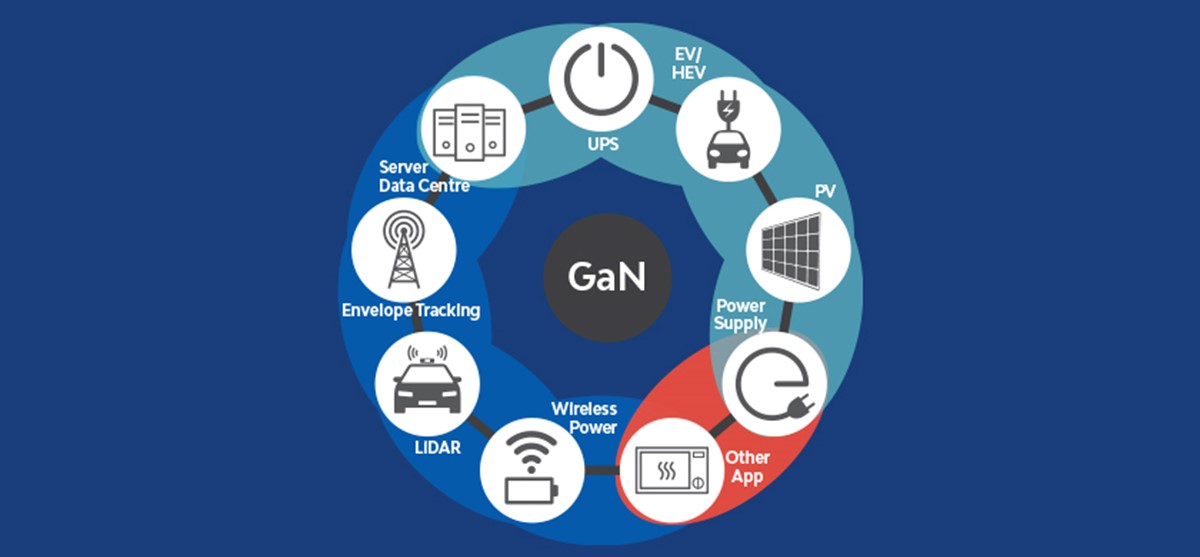

The strong dynamics of the power electronics industry is leading to ramp up in use of WBG1 based materials, in particular SiC and GaN as Si approaches its limits. Devices based on these materials are leading a next generation of energy efficiency and performance due to their intrinsic properties. In particular, GaN on Si power devices are more suitable for high frequency applications while SiC is better for high power density and high temperature inverters.

A market that is booming

Although still relatively small compared to the Si power device market, the SiC market has already reached a relatively significant size compared to GaN due to its more mature technology. In 2017, the SiC power device market was estimated at more than US$300 million, roughly ten times that of GaN power devices. In fact, nowadays we can affirm that end-users are beginning to adopt SiC as the final solution whereas several years ago the market was still very small.

Today, 82% of the SiC market is driven by diodes used in PFC for power supplies, and in hybrid modules for applications such as PV.

Yole Développement (Yole) expects that the transistor market will still grow with a CAGR2017-2023 of 56% with the introduction of these devices into applications such as EV/HEV, including charging infrastructure, partly due to the implementation of full SiC modules. Indeed, this is a hot topic in the overall industry, where we see all the car manufacturers and their Tier One suppliers developing SiC solutions.